Why Billionaire Net Worth Numbers Are More Fragile Than They Look

Discover why billionaire net worth are mostly paper wealth, how market premiums inflate fortunes, and what real assets reveal beneath the headlines and hype

The Number That Sounds Crazy (Because It Kind of Is)

When a headline says someone is worth $800 billion, what does that actually mean?

It doesn't mean they have a bank account with $800 billion in it. It doesn't mean they could write a check for that amount tomorrow morning. It means they own a large chunk of a company and the stock market has decided that company is worth a lot.

That's a very different thing.

The wealth of the world's richest people is almost entirely paper wealth. It lives inside share prices, which are driven not by what a company owns, but by what investors believe it will become. And those two things can be wildly different.

Once you understand that gap, those headline numbers start looking a lot less solid.

Net Worth 101: How the Number Gets Made

The math behind billionaire net worth is actually pretty simple.

Take someone who owns 10% of a company. If the market says that company is worth $1 trillion, that person's net worth is roughly $100 billion. That's the whole calculation which is simply ownership percentage multiplied by market value.

Sounds clean. The problem is the market value part.

Market value is just what buyers and sellers are willing to exchange shares for on any given day. It can and does move billions in either direction based on a single earnings report, a product announcement, or a shift in investor mood. It's not anchored to anything physical. It's a collective opinion.

So is there a better way to measure what a company and by extension, its founder actually has? Yes. And it comes down to two numbers every investor should understand.

Book Value vs. Market Value: The Core Difference

Book value is the accounting version of a company's worth. Take everything a company owns such as buildings, equipment, cash, investments and subtract everything it owes. What's left is the book value, or shareholders' equity. Think of it as the hard-asset floor: what you'd theoretically walk away with if the company shut down today and settled all its debts.

Market value is what investors are willing to pay for the company on the open market. This is almost always higher than book value, sometimes dramatically so, because investors aren't paying for what a company owns today. They're paying for what they think it will earn in the future.

The ratio between the two is called the Price-to-Book (P/B) ratio.

A P/B of 1.0 means the market values the company exactly at what its books say it's worth. A P/B of 10 means investors are paying ten times the book value. They believe future earnings will justify that premium. A P/B of 30 or 40 means enormous expectations are baked in.

Why Different Industries Get Priced So Differently

Not every sector trades at the same multiple, and there's a clear logic to it.

Banks, utilities, and traditional manufacturing companies tend to have low P/B ratios often ranging between 1x to 3x. Their businesses are fairly predictable. The assets are physical and well-understood. There isn't much room for surprise, so the market doesn't price in a big premium.

Technology and AI companies are the opposite. Their real value isn't in physical assets, it's in code, user data, network effects, and software that costs almost nothing to replicate at scale. None of that shows up neatly on a balance sheet. So investors pay a massive premium for the potential, and P/B ratios can reach 15x, 30x, or well beyond.

This isn't irrational on its face. If a company genuinely will generate enormous profits for the next 20 years, paying a large premium today can still be a smart trade.

The catch is that a high P/B ratio is, at its core, a bet. And bets don't always pay off.

When the Bet Goes Wrong

History has a reliable habit of humbling high-multiple sectors.

The most well-known example is the dot-com bubble of the late 1990s. Internet companies were being valued at hundreds of times their book value; some had barely any real revenue at all. Investors were paying enormous premiums for the pure idea of the internet. When the bubble burst between 2000 and 2002, roughly $5 trillion in market value simply disappeared. The companies didn't change overnight. The expectations did.

A more recent example: the SPAC and growth-stock boom of 2020–2021. Fuelled by low interest rates and a wave of optimism, investors pushed the valuations of early-stage tech, electric vehicle, and clean energy companies to extraordinary levels. Many traded at 40x, 60x, even 100x their book value. Then interest rates rose, sentiment shifted, and a large portion of those stocks lost 70–90% of their value in under 18 months. The underlying businesses hadn't collapsed but the premium investors had been willing to pay had evaporated.

The pattern is consistent across every era: the higher the P/B ratio, the more fragile the wealth tied to it. You're not just owning a company, you're owning a story about the future. And stories can change.

The Liquidity Problem Nobody Talks About

Here's a layer to this that rarely gets discussed in the wealth headlines.

You and I can log into a brokerage account, sell shares, and have cash within a few days. No friction, no complications. For regular investors, market value and accessible wealth are roughly the same thing.

For someone who owns 15%, 30%, or 40% of a company, it's a completely different situation.

When a major insider starts selling large blocks of stock, the market notices immediately and it reacts. Other investors read it as a warning sign and start selling too. The price drops. The more shares being offloaded, the further the price falls, which means later sales happen at a lower price than earlier ones. It becomes self-defeating.

Regulations add another layer. In most markets, insiders are required to disclose planned trades in advance, giving other participants time to react. Many founders also operate under contractual restrictions on how much they can sell in a given period. There are board considerations, reputational signals, and in some cases tax structures that make large-scale selling complicated and costly.

What this means practically is that a billionaire's stated net worth is really a theoretical ceiling of what they'd get if they could sell everything at today's price without moving the market at all. In any realistic scenario, a large liquidation would yield considerably less.

Their paper wealth is real. It's just not nearly as accessible as the number suggests.

The Real Numbers: What Billionaires Actually Own

This is where it gets genuinely interesting. When you swap out market valuations for actual book values, what these companies hold after subtracting all liabilities, the picture changes dramatically.

The estimates below are based on Q1 2026 balance sheet filings and each person's known ownership stake:

Let that sink in for a moment.

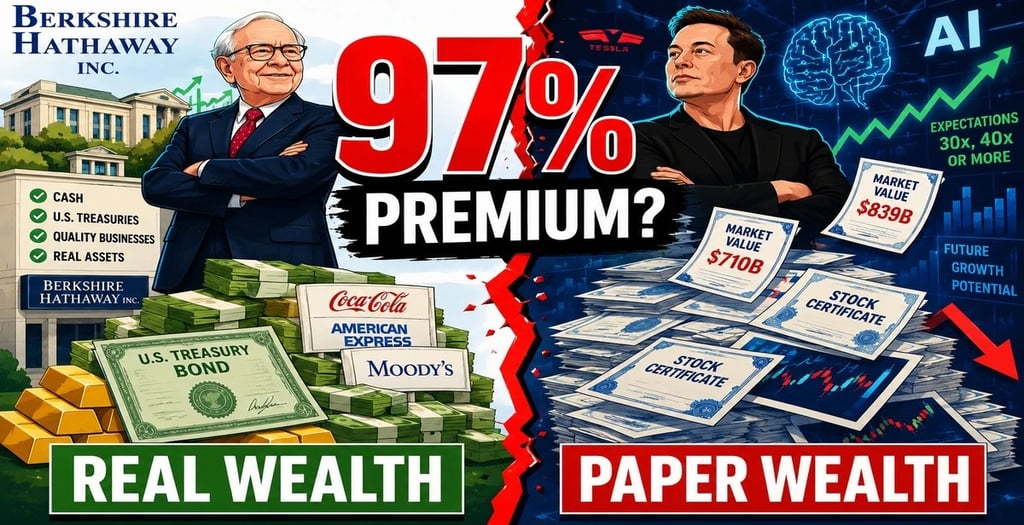

The person who looks the least impressive on the market-value list is sitting on the most solid wealth. The person who tops the list by a historic margin has roughly 97% of his stated net worth sitting in market premium which are expectations that investors have piled in, not assets the company currently holds.

That's not an accident. It's a direct reflection of how differently these businesses are structured.

So Who Actually Holds Real Wealth?

The table makes it clear, but the why behind it matters just as much.

Berkshire Hathaway, the company most of Warren Buffett's wealth is tied to, is built fundamentally differently from the tech giants that dominate the wealth rankings. Its balance sheet is stacked with cash, government securities, and stakes in established, cash-generating businesses. There's no massive premium priced in for future moonshots or AI breakthroughs. The gap between what Berkshire actually owns and what the market pays for it is narrow and that narrow gap is exactly what makes it more stable.

His wealth is also structurally more liquid than most. A diversified holding company can reduce positions gradually, sell parts of its portfolio over time, and manage a wind-down without triggering a collapse in its own valuation. It doesn't depend on a single stock staying elevated forever. That's an enormous practical advantage that rarely makes it into the net worth conversation.

Compare that to founders whose entire paper wealth is a single concentrated stock trading at 30x or 40x its book value. Those numbers can shrink by hundreds of billions in a few bad weeks. The companies are real, the assets are real but the degree of certainty between the two situations is not even close.

Real wealth isn't just about size. It's about how much of it is grounded in what already exists versus what the market is hoping will exist someday.

The Bottom Line

Those enormous net worth figures in headlines aren't lies but they're not the complete picture either.

They tell you what the market believes someone's stake is worth today. They don't tell you how much of that is backed by hard, tangible assets. They don't tell you how easily it could be converted to cash. And they don't tell you how much would survive if investor confidence decided to take a turn.

Book value isn't a perfect measure on its own; no single number captures a business fully. But it grounds the conversation in reality. It separates what's actually there from what investors are hoping will be there.

The next time you see a jaw-dropping net worth headline, ask one simple question: what's the P/B ratio?

That one question changes how you read those numbers forever.

Note : All net worth figures referenced in this article are based on publicly available market data and Q1 2026 SEC balance sheet filings. Figures are estimates and subject to change with market movements.

MacroUTC

Newsletter

© 2024. All rights reserved.

Contact